In neighboring Bangladesh, female workers have played a crucial role in helping develop the garment industry—although the country’s factories have drawn charges of safety issues and worker exploitation. Bangladesh had a female labor-force participation rate of 38% last year, up from 28% in 2000. Its GDP per capita has surpassed India’s since 2019.

Economists say compared with India, Bangladesh has looser labor laws that have allowed factories to expand quickly and doesn’t have as many strong caste rules that encourage social conformity.

Reading about what has happened in urban Bangladesh due to the employment of young women in textiles is like reading about New England towns in the early 19th century. It’s basically history repeating itself. As I was reading the article I did wonder about caste and communalism; in many nations worries about who young women would meet at factories in particular was and is a massive concern. Could this really be an issue?

Over at his Substack, Noah Smith has a pretty bullish take on India, Here…comes…INDIA!!!:

The United Nations estimates that India has now surpassed China as the world’s most populous country — or, as we colloquially say, the world’s “largest” country.

Obviously, crossing this threshold doesn’t mean much in practical terms. Being a tiny bit bigger than China doesn’t really change anything, and India has just about as many people as it did a year ago. But the flurry of news stories accompanying the event is a wake-up call for the world: India has arrived on the world stage, in a big way.

What does that mean? Well, a whole lot of stuff. More stuff than I can summarize or even mention in a single blog post. There was a quote attributed to Napoleon two centuries ago: “Let China sleep, for when she wakes, she will shake the world.” Well, China did wake up, and the world has been shaken. The whole economic landscape of the planet, the geopolitical balance of power, and even the Earth’s environment have been irrevocably changed in the last three decades by the addition of 1.4 billion human beings to the ranks of the (more or less) developed world. Now India brings another 1.4 billion, eager to join those ranks. Get used to seeing a lot more graphs with this basic format…

It’s a long post, but I think the major takeaway from the viewpoint of an economist is agglomeration. The co-location of producers and consumers and resources at such massive scale nations like China, India and the USA, result in a level of synergistic economic growth and power that smaller nations cannot match structurally. This is probably one reason that Britain punches below its weight vis-a-vis the US, it cannot scale.

But Smith is aware of human capital concerns, and this is probably the a signifier of the number one issue: Worthless Degrees Are Creating an Unemployable Generation in India. Fake credentialing just means firms will have to re-train or do their own intake (the obsession with credentialing shows up in funny ways on even on this blog; I don’t care what your credential is if you are a moron, something is common-sense to Americans working in tech).

Another issue that is focused on in the post is that India needs to focus on productivity growth through manufacturing. I actually thought a bit about India when I read this long and excellent piece in Palladium on the century-long failure of the British ruling-class on updating their nation for the 20th century.

A giant Indian conglomerate couldn’t stop the freefall in its shares and bonds set off by an American short seller in what has grown into a bitter fight over the empire created by one of India’s richest and most politically connected businesspeople.

Adani Group, an energy and infrastructure company, released its 413-page rebuttal to the short seller’s claims just as the trading week began in Asia. Investors weren’t convinced and dumped shares of the company on Monday, bringing the total value lost to $64 billion since last week.

The fight could have wide implications for India’s power industry and for its transition to clean energy. It has also caused billions of dollars in losses for Indian investors who have helped drive up the company’s share price to stratospheric levels.

Most large companies hire credible, well-known external auditing firms in order to give investors confidence that their financials are being independently reviewed by a capable team.

Given the complexity of Adani Total Gas and, particularly, Adani Enterprises, with 156 subsidiaries and many more affiliates and joint ventures, one would expect a large, highly experienced team to be monitoring its labyrinthian corporate structure.[62]

But Adani Group has apparently shunned this approach, choosing a tiny auditor named Shah Dhandharia to oversee the audits for these two public companies.

Shah Dhandharia’s website has gone offline during our investigation and now appears to have no website. Archived versions of the website as of February 2020 show that the firm was comprised of only 4 audit partners and 7 support staff.[63]

Of the partners featured on its team page, we found that 3 were in their 20s – hardly the level of experience or seniority needed to seriously scrutinize one of the world’s wealthiest and most powerful businessmen.

Apparently, the Adani group has a 413-page rebuttal to the short-sellers. Rebuttals often take more time/space…but I not going to lie, I am not surprised at the length here…

(though some short-sellers have done sketchy things, my own view is short-sellers are an essential part of af functioning market and discourage crony-capitalism)

The Indian capital, which just weeks ago suffered the devastating force of the coronavirus, with tens of thousands of new infections daily and funeral pyres that burned day and night, is taking its first steps back toward normalcy.

Officials on Monday reopened manufacturing and construction activity, allowing workers in those industries to return to their jobs after six weeks of staying at home to avoid infection. The move came after a sharp drop in new infections, at least by the official numbers, and as hospital wards emptied and the strain on medicine and supplies has eased.

Life on the streets of Delhi is not expected to return to normal immediately. Schools and most businesses are still closed. The Delhi Metro system, which reopened after last year’s nationwide lockdown, has suspended service again.

But everyone has to focus on the future. So what’s going on? How’s Modi’s going to supercharge the economy? I’m not Indian, I’m American. A strong India is good for America. An economically vibrant India is good for humanity.

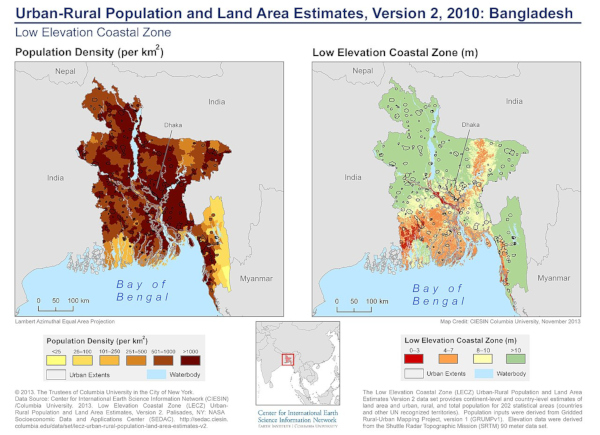

In the comments below there is some mention of the problems that Bangladesh will face due to increases in global sea level. The hypothesis is that there will be a mass migration to India as Bangladeshis flee low-level zones which are going to be inundated. I don’t think this is capturing the real issue: if millions of Bangladeshis are still subsistence farmers on marginal maritime zones then there has been a massive development failure.

Even extreme sea-level scenarios by 2100 posit a 2.5-meter rise, which means only a small proportion of the territory of Bangladesh would be inundated. If by 2100 Bangladesh is not a predominantly urban society after 80 years of economic development from 2020, there are much deeper structural problems to deal with than climate change.

Development and wealth change the downsides of risk a great deal. The 1970 Bhola cyclone caused hundreds of thousands of deaths. Something that is unlikely to be replicated in the region for various reasons (e.g., information technology and coordination are far better!).

I’ve been paying attention to climate change since the late 1980s. As someone whose family is from Bangladesh I have been very worried…my image in 1990 was of peasants fleeing inundated paddies. But things have changed a great deal. In 2020 nearly 40 percent of Bangladeshis live in cities. By 2100 a substantial majority should…

Bangladesh’s per capita gross domestic product (GDP) is now higher than most Indian states in eastern and northeastern India, with the exception of small hill states such as Mizoram and Sikkim. According to the data from the International Monetary Fund (IMF), Bangladesh’s per capita GDP was $1,905 in 2019, against West Bengal’s $1,566 in 2018-19 (FY19) — economically the most developed state in eastern India.

Bangladesh is not really comparable to India, which is a diversified economy that is more than an order of magnitude larger. But, it is comparable to West Bengal. On economic matters, I am broadly sympathetic to right-liberal economics, so I’ll spare you my interpretation of what’s going on.

Do state capacity and policy really matter when it comes to wealth among regions in South Asia ? Or is prosperity today determined largely by a mixture of geographical and historical factors ? South Asia as a unit is a reasonable region to study because the introduction to modernity in this entire region was mediated by the British Empire.

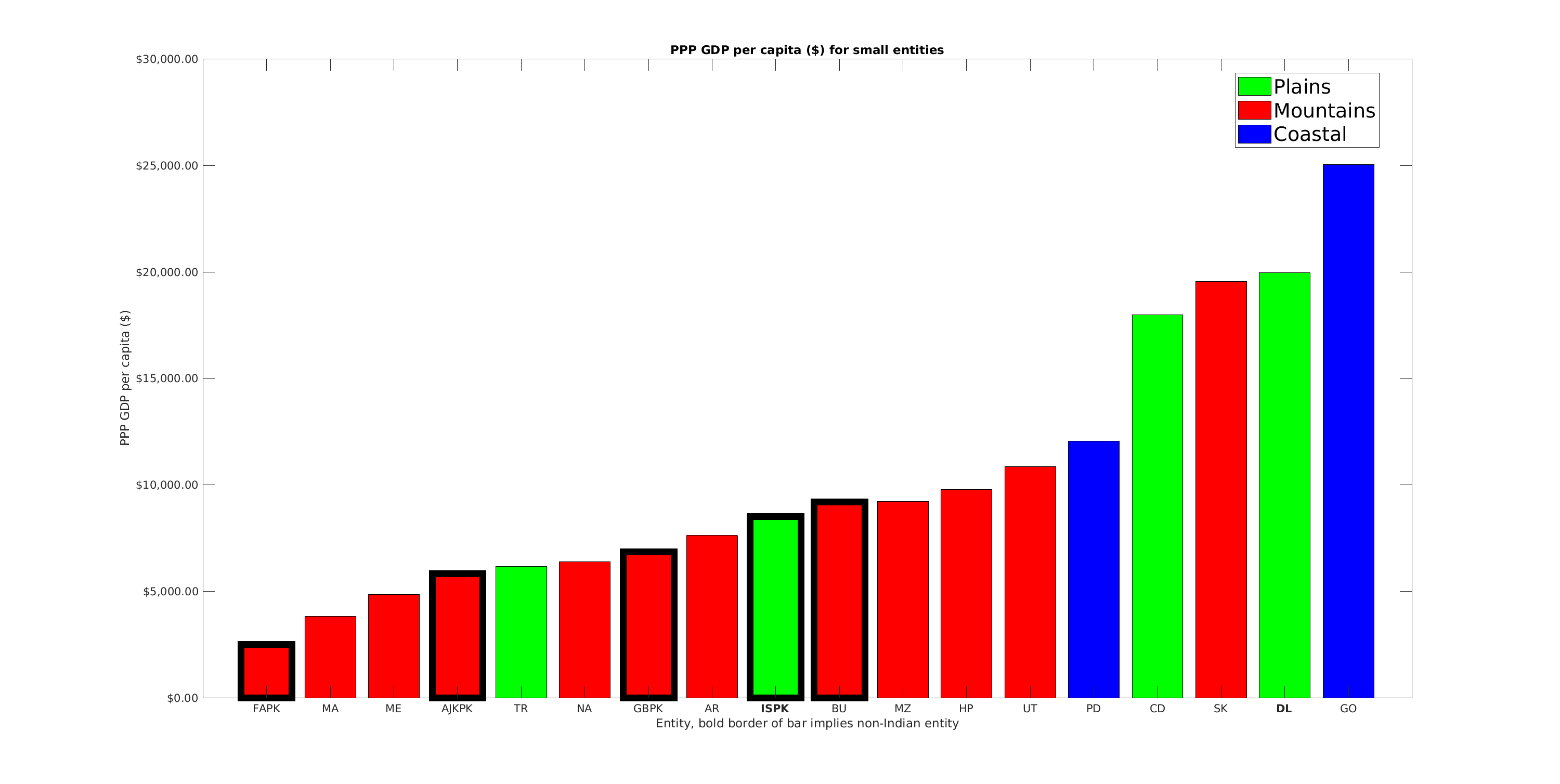

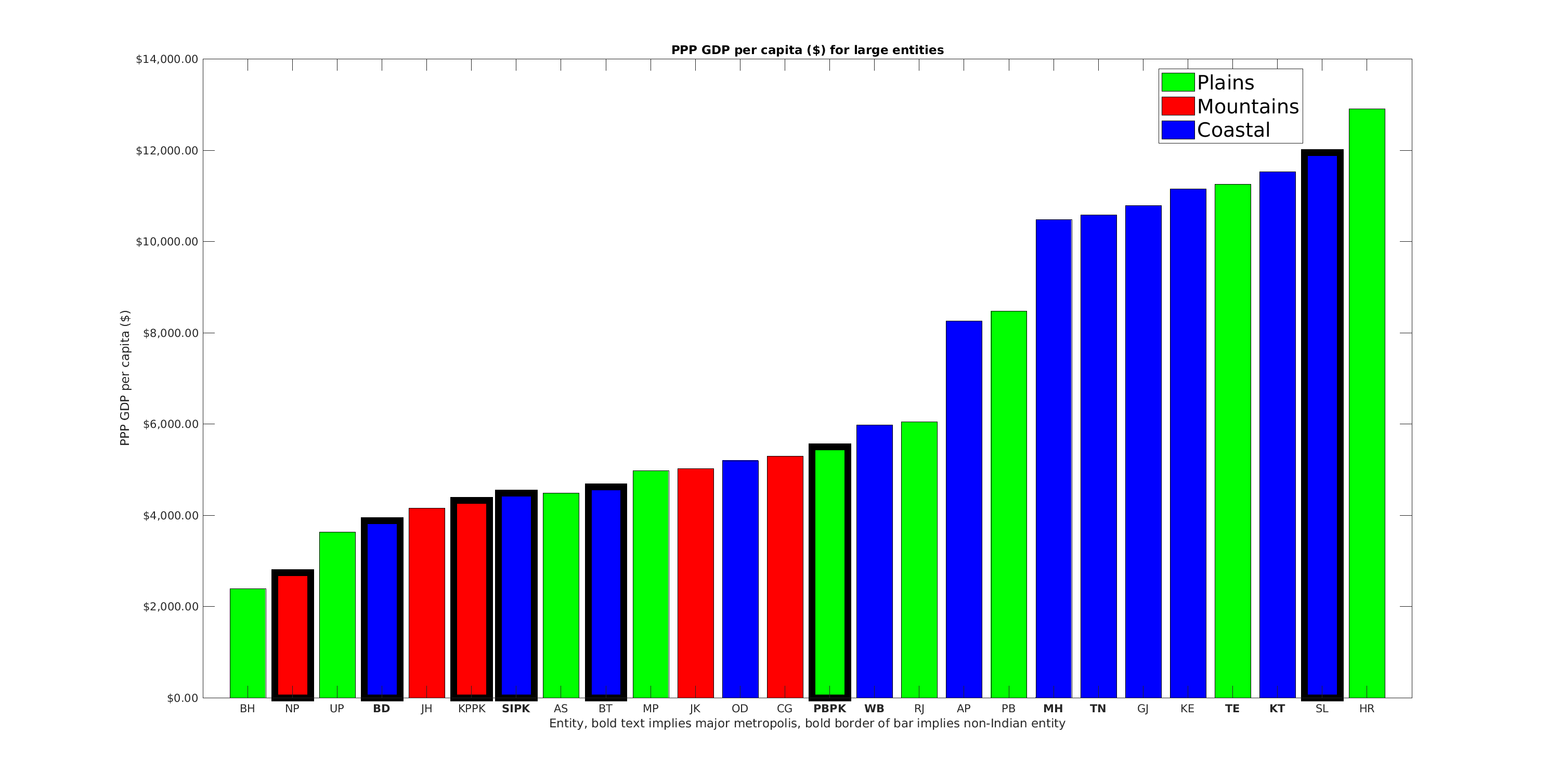

Seen in the two figures below are GDP per capita ($ PPP) figures for smaller (< 20 million population) and larger (> 20 million population) regions. The entities include the nations of Bhutan, Nepal, Bangladesh and Sri Lanka, states and union territories of India, and provinces of Pakistan. Some notes about the two figures:

Green bars denote plains regions, red mountain regions and blue coastal regions.

Bold x-axis labels indicate entities with major metro areas.

Bold borders around bars indicate non-Indian entities.

GDP per capita ($ PPP) of smaller political entities (< 20 million) in South Asia. Indian states, Pakistani regions and nation of Bhutan. Bold x-axis label denotes presence of metro area. Bold border of bar indicates non-Indian entity.GDP per capita ($ PPP) of larger political entities (> 20 million) in South Asia. Indian states, Pakistani provinces and nations of Nepal, Bangladesh and Bhutan. Bold x-axis label denotes presence of metro area. Bold border of bar indicates non-Indian entity.

There are roughly five bands of wealth we can identify:

Rich smaller entities of India: Goa, Delhi, Sikkim and Chandigarh. These have GDPs of around $20-25000.

Richer large entities consisting of Indian states and Sri Lanka. GDPs are around $10-12000, and these are predominantly coastal regions.

Succesful agrarian states of India (Punjab and Andhra), mountainous states of India (HP, UT, MZ), Pakistan’s capital Islamabad, and country of Bhutan. GDPs between $8-10000.

Interior Indian states and Odisha, along with all Pakistani provinces. This is the South Asian mean performance of around 4-6000$.

Poor regions: Indian states of UP, Bihar, countries of Bangladesh, Nepal, Pakistan’s remote area of FATA and India’s remote state of Manipur.

Clearly being on the coast and having a major city help in a major way. In this context, there are three regions which are major disappointments, India’s West Bengal, Bangladesh and Pakistan’s Sindh. All three are on the coast, have major metropolitan areas and even have rich agricultural lands. But their economic performance is significantly below potential.

On the other hand, the economic star of the subcontinent is the Indian state of Haryana. It defies every convention, its not on the coast, lacks a huge metro region and lacks abundant rainfall. But it excels in every aspect of economic activity, its agricultural productivity is second only to Indian Punjab, its industries are varied and well developed and its service sector is a leader in India along with Karnataka. Gurugram hosts genuinely innovative startups, home to at least 7 of India’s 30 unicorns.

An interesting comparison is that between the state of Punjab and the Pakistani province of the same name. Indian Punjab is richer despite lacking a metro area. But there is a convergence in certain aspects. These are rich agricultural areas, with strong remittance networks but they both might lack industrial entrepreneurs.

Bihar, Nepal and Eastern UP together continue to be home to the largest concentration of poor people on planet Earth. This is an isolated region, with no major cities, neglected by every Indian political entity for many centuries now. The Modi government’s national waterway one has already connected the region upto Varanasi to the ocean, upstream will be a technological challenge. Nepal, can look to Indian states like Uttarakand and Himachal for an effective growth strategy.

Although geography and history play a major role, the example of Haryana shows that those factors can be overcome. Market access, aggregation effects and the presence of mercantile communities are the key variables that determine economic performance.

8% vs. 3%. From a geopolitical perspective at current rates of relative stagnation India’s Pakistani problem will “solve” itself as the Islamic Republic is turning into a macroeconomic midget. All of the geopolitical posturing will be irrelevant if the Pakistani polity doesn’t get its structural house in order (e.g., shift away from the oligarchy).