This post is published on behalf of Yajnavalkya – Medium

————————————————————————————-

A GST terror story

Modi has announced during his Independence Day speech that he would be going for sweeping reforms of GST by Diwali. The central piece of the reform would be reducing the number of rates from 4 to 2. A lot of people – both experts and non-experts – have been advocating a single/dual rate regime as a magic bullet for the GST mess.

But is it? Let me start by narrating a GST horror story. Some GST basics first: GST is a value-added tax. Assuming a product has 10% tax, Manufacturer A sells the product to wholesaler B for Rs. 1000 (pre-tax). B pays A Rs.1000 + Rs. 100. B then sells the goods to Retailer C for Rs. 1050 (pre-tax) and C pays B Rs. 1050+Rs. 105. Now since B has already paid Rs. 100 as tax to A, he is required to deposit only Rs.5 to the exchequer. The Rs.100 that he paid the manufacturer is termed as ‘Input Tax Credit’ or ITC.

There are some elaborate ways of defrauding the system of taxes involving ITC which is also facilitated by loopholes in the tax filing process – discussing that would require a 5000-word post, so I will desist. But for those interested, you can read up about bill trading. One of the ways in which the system combats this menace which potentially causes trillions in tax losses, is Rule 86-A, which empowers the taxman to block ITC of any businessman if he has “reasonable cause” to believe that the ITC was fraudulently availed.

Ok, now on to the story. A few months back, a bunch of businessmen operating in the steel sector in my city – including one of my personal acquaintances – were slapped with notices under this rule, blocking ITC aggregating to Rs.60 million, for transactions related to the period 2021 to 2024. The stated reason – Supplier X from whom these people had purchased goods (and taken ITC credit) was declared to be “non-existent” and hence all those purchase transactions were fake. But here is the thing – the supplier was very much “existing” during the said period. There was concrete evidence of the same – power bills for the factory running into tens of millions, his GST filings, company annual returns, income tax returns and so on. The supplier had closed down his business in early 2025, not in small part due to the pain of GST terror and compliance burden. The panicked recipients of the notices went to meet the taxman, taking along the supplier and with all the aforementioned evidence. The taxman was unmoved. So next they moved to the court but the latter dismissed the petition asking them to exhaust the appeals process via the department first. Before filing an appeal, 20% of the blocked ITC needs to be deposited. The legal costs in this case would have added another couple of million Rupees. Having figured out that legal process was not worth the effort, the group sent a message to the taxman requesting a deal. Initial demand-Rs.12 million. After lots of hard bargaining, it was finally settled for Rs.8 million..

There is a lot to unpack here. I will leave out the technical and legal aspects.

One, there is just a stunning level of discretionary powers vested with our tax babus, who exercise it with a singular focus on national building and punishing the tax evaders in a parasitical manner – for personal enrichment and of their political bosses – indulging in rampant rent-seeking and shakedown of the taxpayers. They have the power to severely disrupt the business operations of an average businessman for the most frivolous of reasons. And there is very little downside for such abuse of power.

Two, the presumption of guilt with regard to ITC flouts all principles of natural justice. In this case, for example, all the customers of the Supplier X are assumed to have colluded with him in the “fraud”. The law leaves no scope for a presumption that many customers might have been unwitting victims of the fraud. And this rule is not just applicable in case of fraud. Even in case of legitimate transactions, if the supplier fails to deposit the tax paid by the buyer, the department can go after the buyer for the unpaid dues (and this rule persists even after court judgements have held it to be untenable).

Three, the corollary to the above is that the primary responsibility for tax evasion/fraud across his supply chain rests with the businessman. In other words, the tax department has outsourced its job of enforcing tax compliance on to private citizens. The repeated message from Nirmala Seetharaman and her finmin babus to industry groups complaints regarding ITC has been very clear – the businessmen must ensure that they trade only with genuine parties.

Last, the taxman can go back up to 7 years of transactions for uncovering evasion/fraud. In the above instance, for example, ITC starting 2021 was reversed. Imagine the level of uncertainty the system is placing a businessman in if he has to keep worrying about establishing the genuineness of every other transaction done years back.

When we have these periodic news reports of the department busting a GST scam and people cheer on against this war against tax evasion, I worry about the 1000s of hapless businessmen who are caught in the crosshairs for no fault of theirs.

Reduction in slabs will be touted as a big-bang reform…it is not

As I mentioned earlier, the reduction in slabs from 4 to 2 is going to be the core part of the second-generation GST reforms. Whether a reform is big-bang or not should be judged based on two parameters – A) risk of execution – primarily political and economic risks and B) how far-reaching the impact of the reform is.

Politically, slab reduction is going to be popular as rates of many goods, especially big ticket ones, will come down meaningfully. So it is a good political sell. With the GST compensation cess Fund getting freed up, the transition to two rates – reportedly proposed to be 5% and 18% – can be done in a revenue neutral way. That also makes it a politically easy thing to execute as ruling parties in the states would not want to be seen as opposing a move benefitting consumers. Of course, one should totally expect oneupmanship from opposition parties – why would they let Modi take all the credit?

In my view, the impact of a reduction in slabs is vastly overstated. There are two tangible benefits as far as I can see – one, it reduces the problem of inverted rate structure and two, it forces rate rationalization (i.e a policymaker has only two choices for rates instead of four) and in turn, reduces classification related disputes. In a world where the entire business accounting is computerized, for a business to be set up to handle multiple rates is a trivial job. If you talk to business folks, you will find very few who think of multiple rates as even a top 5 problem within GST. So it’s bemusing when it is bandied about as a magic bullet in GST reforms in mainstream discourse.

None of the issues in the aforementioned GST horror story are resolved even the tiniest bit because of rate rationalisation or a two-slab structure. The entire steel sector has a single GST rate of 18%.

Not that any of this will stop Modi and his party from chest thumping the slab reduction as a revolutionary reform. Well, one really cannot begrudge politicians indulging in politicking but as a long time BJP supporter, it would truly be disheartening if yet another opportunity for meaningful reform is missed, camouflaged by soaring rhetoric and bombast. And mind you, I say it not as a Modi critic – there are posts in this website where I have profusely praised Modi for his fiscal Tapasya during the second term.

The other “pillars” of proposed reforms indicate a depressing absence of ambition

The Finance Ministry’s PR following the PM’s speech talks of three pillars underpinning the GST reforms consisting of 9 actionable areas. A majority of it revolves around rate rationalization and reduced slabs. But look at the 3 points related to “Ease of Living” (I think they meant ease of doing business) – it talks of making GST registrations and refunds easier. These are pretty much the two most basic aspects of a semi-functioning tax system and this government is advertising fixing this in the 9th year of GST as a major reform!! I hear that the going rate for getting refunds processed in my state is 5-6%. You can read numerous cases in social media of registration applications being rejected for frivolous reasons.

That said, one of the items does hold some promise – a commitment to stability and predictability….one can only hope that some lessons have been learnt from the 100s of amendments and rule changes over the last 8 years.

Real reform would be to curtail babudom’s discretionary powers and reduce compliance burden

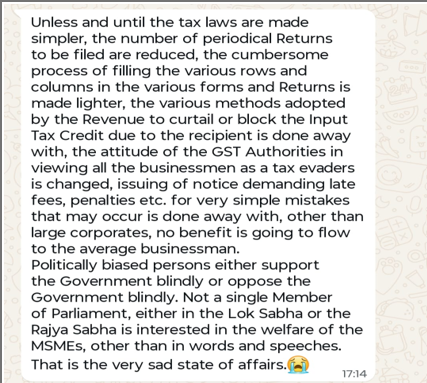

I asked a popular GST consultant known for his work for MSMEs what he thought of the shift to two slabs. He was totally dismissive of any benefit for his clients. I am quoting his Whatsapp reply below:

The message points out to two broad pain points – one, high discretionary powers for babus, especially in their ability to withhold the taxpayer’s ITC or refunds. Two, high compliance burden. It goes without saying that the latter only facilitates the babus to extort further.

An administration genuinely serious about reforms and in improving ease of doing business would, at least start by indicating that they understand the problem. I have seen no evidence of such awareness so far. Admittedly, actual execution is extremely fraught, both politically and administratively – a loosening of babu’s powers and compliance burden, especially the former, will likely result in sizeable leakage in tax revenues near term; not least because of sabotage by babus. This will not be palatable to the states. A real reform push by Modi would therefore involve nudging the states in this direction backed by some monetary incentives to compensate revenue loss. At any rate, Modi has enough political capital to push BJP ruled states in this direction. That is not to say that Modi should jump right in with radical changes. That would obviously be destabilizing to the system. But start by nibbling at the corners, curtail some of the most egregious aspects of discretionary powers, ease up on some of the silliest compliance requirements.

Modiji, let the businessmen breathe please, before we start talking of kindling the animal spirits!

Postscript 1

The stress faced by the MSMEs can be understood in terms of the changing nature of the political economy and the relative loss of the political heft of MSMEs. A decade or so back, perhaps the buyer group in my story (some of whom are local elites and multi millionaires) would have tried to resolve the issue by connecting to a minister via the local MLA. But they do not have that kind of leverage today. The minister is playing at a different level – dealing with large corporates for amounts in the tens of billions.

Postscript 2

A major structural reason for GST being such a mess in India is because the tax rates are very high – bigger the GST pot, higher the motivation to extort and rent-seek. A moderate tax level would automatically bring down the level of bureaucratic friction. India is a major outlier in terms of its tax structure – 2/3 of our taxes are derived from consumption taxes and only 1/3 from direct taxes. For many other comparable economies, the ratio is the reverse. On balance, tax terror on direct taxes is a lesser evil than on GST considering the latter is extremely disruptive not just for the individual business, but for players across the supply chain.

the problem is very old as can be seen in ‘yes minister’ serial. bureaucracy has no stake in changing the system which gives them enormous powers. one should experience an ‘i t raid’ to see this. after all they stay for 35 years whilst a politician stays for max 10years.

prof.vaidyanthan has said repeatedly that more than 200 rules can be struck off so that doing small business becomes easy and takes away the powers of the officials.

modi govt has a golden chance to do real reforms at the lower, working level. for this we need a minister who can cut through the web of rules and free business. nirmala sithraman is not one such individual. modi is also a stateist. the state governments while blaming gst etc are not willing to give away their powers.

recently a guy near our place , who has a milk kiosk got a rs 13 lakh tax notice. he has since closed shop and run away.

india needs a margaret thatcher in this regard.

I don’t know if a Thatcher is possible; the problem is trying to win the next election cycle.

Yes, but that is part of the trouble, if the Modi govt creates economic discontent that means electorally they go in for polarization. The only way India works harmoniously is economically. Trump isn’t making it easy either. The AAP had this great ombudsman idea (which they made central to their manifesto and never implemented, dismantling their own internal ombudsman system first).

fascinating piece; I had no idea that the tax regime was this complicated.

I notice this in airports, there is ALOT of bureaucracy, in one flight my ticket was checked something like 7-9 times!

yes – I think wealth redistribution is important in India but what I find interesting is that Pakistan was exactly opposite but has turned out much worse.

apparently tariffs coming in now