On February 28, 2026, the United States and Israel struck Iran.

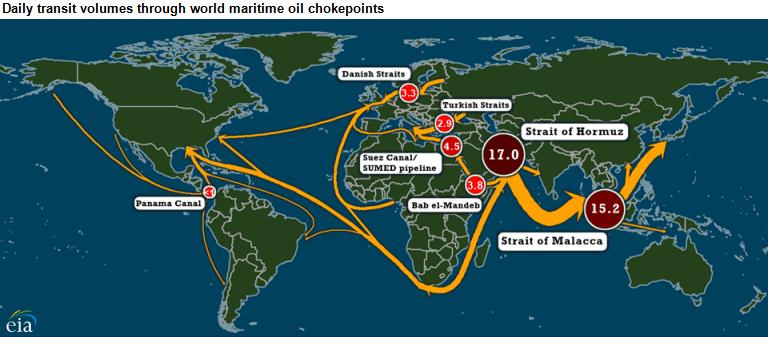

They hit fuel depots, missile sites, command infrastructure. Within seventy-two hours, the Strait of Hormuz, twenty-one nautical miles at its narrowest, carrying twenty percent of the world’s oil, closed. It has not reopened. Everything that follows from that sentence is not speculation. It is arithmetic.

The Price

Oil was at sixty-five dollars a barrel when the bombs fell. Within days it touched one hundred and twenty. Analysts at Kpler said publicly that if Hormuz stayed shut through March, one hundred and fifty was not a ceiling. Barclays agreed. The IEA called the disruption the largest in the history of the global oil market, twice the scale of the 1956 Suez Crisis. People heard those numbers and thought: petrol prices. School run. Heating bills. They were thinking too small.

The Cascade

Oil is not just fuel. It is the circulatory fluid of the entire industrial world. When it doubles overnight, everything that moves, everything that is made, everything that is insured, financed, or shipped reprices simultaneously.

Marine insurance becomes unwritable. Trade credit freezes. Every CFO at every company in every sector looks at their cost assumptions, built at seventy dollar oil, and cancels the next quarter’s capex in the same morning meeting. That coordinated freeze is not a symptom of recession. It is the recession, arriving before a single GDP figure confirms it.

The banks come next. Energy loans, airline debt, shipping company bonds, all underwritten at sixty to eighty dollar oil. At one hundred and twenty sustained, covenant breaches begin quietly. Not crashes. Tightening. The marginal credit that keeps service businesses alive stops flowing.

Then the Gulf sovereign wealth funds. ADIA. PIF. QIA. Mubadala. Two to three trillion dollars in global assets, equities, real estate, private equity, deployed as patient capital into Western markets for fifteen years. They are nominally richer at one hundred and twenty dollar oil. But their export infrastructure is disrupted, their domestic spending obligations spike immediately, and their liquidity needs arrive precisely when their asset values are falling.

The moment even one major fund moves from net buyer to net seller, it removes the price support it has been providing silently for years. Other funds follow. The risk premium they have been suppressing across global asset classes reasserts overnight.

This is not the 2008 financial crisis. That was a fire in the financial system’s wiring. This is the fuel supply to the engine failing. Different category. Larger consequences.