In the run up to Indian parliamentary elections in 2024, there is excitement in some sections of social media about “freemarket” ideas espoused by C Rajagopalachari (Rajaji) and the Swantantra Party he helped found in 1959.

Sharing a piece here I wrote on Rajaji’s ideological relevance in contemporary politics. This was written after visiting and reporting from the many institutions he built pre and post 1947 for the now defunct Pragati Magazine in 2018.

And the food-and-agriculture-focussed independent media platform called the ThePlate.in I run.

Here goes…

Rajaji: Our Forgotten Hero

Among the leaders in the front ranks of the freedom movement, and those counted as the makers of modern India, Chakravarthi Rajagopalachari (Rajaji) is perhaps the man most forgotten. Gandhi is the ‘Father of the nation’; the very existence of India as a modern democracy, and lately all its faults—from clogged drains to currency fluctuation—are credited to Jawaharlal Nehru’s side of the ledger; the race to usurp Vallabhbhai Patel’s legacy has given India a Guinness record for the world’s tallest statue; Bhimrao Ambedkar is not only a Moses-like lawgiver who framed the constitution but also the messiah of marginalized; Maulana Azad, now firmly located in Indian-Muslim politics, finds an occasional ode to his prescience about the fallacy of Pakistan and subsequent fate of subcontinental Muslims. Rajaji is less lucky than Azad. Continue reading Rajaji: Our forgotten hero

The story of twenty-five -year-old Narayan Lal Gurjar might not be out of place in Bollywood.

The playful experiments he conducted in his father’s small farm as a teenager in Kerdi, a village of 300 with 40 homes in Rajsamand district in southern Rajasthan, is the foundation for his patents and the agriscience startup incubated by Okinawa Institute of Science and Technology that has attracted investments from well-known Japanese venture capital firms such as Beyond Next Ventures and MTG.

And all this before he turned 23.

Gurjar’s firm EF Polymer (EF stands for eco-friendly) headquartered in Okinawa with manufacturing plants in Udaipur makes super absorbent polymers (SAP) from orange and banana peel that has the potential to help millions of small farmers in arid and water scarce regions across the world harvest better yields.

Come summer, Indians engage in a unique mango one-upmanship: Alponso or Langda; Ratnagiri or Devgarh Alphonso; Gujarati Kesar or Banarsi Chausa. If you ask me, this kind of mango tribalism is trite. The mango season is short. Eat whatever you can find.

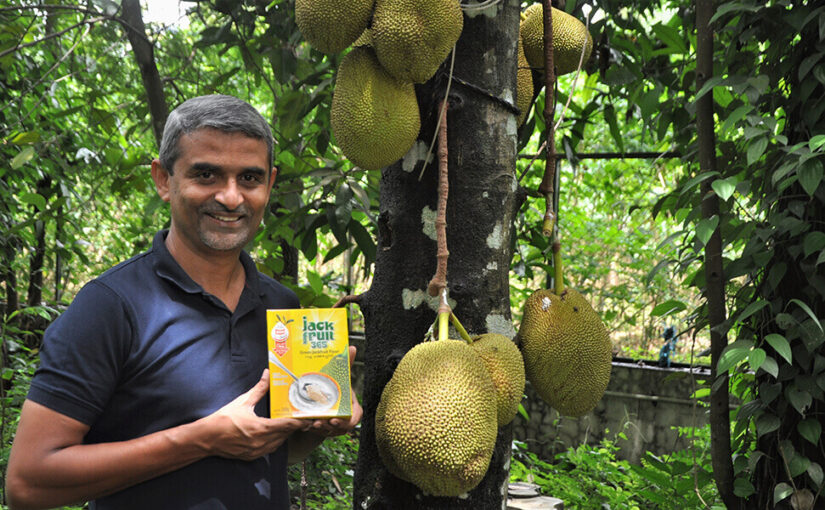

But this is also the season of jackfruit, a fruit far more complex in flavour, and a veritable super food that Indians in its native land love to despise. Jackfruit of course has an exalted status in traditional Tamil literature, alongside banana and mango. Jackfruit can grow prolifically anywhere in peninsular India and the mid-to-lower Gangetic belt, pretty much.

I’ll share a couple of The Plate’s jackfruit stories here.

The right socio-economic conditions, availability of trainable talent, clement weather all year-round and a pioneering entrepreneur’s vision to harness it all setting up a sunrise-sector business turns a dozy place into a prosperous hub of startups. This isn’t yet another paean to Bengaluru’s status as the ‘Silicon Valley’ of India. It is the story of a place smack in the geographical centre of Karnataka, 300km to the northwest of Bengaluru called Ranebennur that’s the epicentre of India’s hybrid vegetable seed production.

Since seeds are the most critical and fundamental unit of input in agriculture, it would not be an exaggeration to call such a place ‘startup town’.

Seeds of success

Ranebennur is where India’s largescale, commercial production of hybrid vegetable seeds began in the late 1970s. Today, most major national and multinational agriculture companies from Syngenta to Pioneer to Namdhari have operations in the region. The farmers in this small region produce roughly Rs 500-crore worth of hybrid seeds of vegetables such as tomatoes, chillies, brinjal, okra and assorted gourds.

Such is the economic impact of hybrid seed companies on the local economy that it is common to find homes bearing homage to them. A seed company’s name inscribed in concrete suffixed with the word ‘krupe’ (benevolence) on the forehead of concrete homes painted in bright Vaastu-compliant colours ranging from parrot green to lemon yellow and Barbie pink isn’t a rare sight.

All of it is thanks to Manmohan Attavar a pioneering horticulture scientist and entrepreneur who must rank alongside MS Swaminathan and Verghese Kurien in the pantheon of modern India’s agriculture renaissance figures.

Manmohan Attavar, a pioneering scientist who created India’s first commercial tomato and capsicum hybrids

Read the full story here about how a pioneering Indian scientist-entrepreneur turned a non-descript town in Karnataka into India’s vegetable garden.

Follow ThePlate.in to understand India from farm to plate!

On the occasion of India’s 65th anniversary of Independence, television channels CNN-IBN (now CNN News18), History Channel, and Outlook magazine jointly ran an audience poll, steered by a panel of “experts”, to ascertain the ‘Greatest Indian after Gandhi’.

Mankombu Sambasivan Swaminathan, who passed on at the age of 98 on September 28, 2023, barely made it to a shortlist of 50, let alone the Top 10 that contained Sachin Tendulkar and Lata Mangeshkar in a club overwhelmingly comprising politicians.

Such lists are gimmicks anyway and a result of political partisanship, recency bias and media narratives.

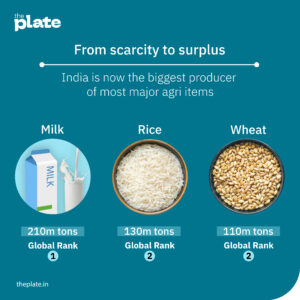

In this writer’s view, with no disrespect to those of yours, there isn’t anyone more worthy of the tag ‘greatest Indian since Independence’ than Dr MS Swaminathan. He provided the bedrock of science and built institutions up from scratch with scant resources to usher in the Green Revolution. His contributions made India not just food self-sufficient, helped 800 million poor escape hunger, but also turned it into a leading producer of every major agricultural commodity.

Faith and food

Swaminathan can be seen as the male embodiment of Annapoorna, a form of Parvati, the Hindu deity of food and nourishment, holding in one hand a Leitz binocular research microscope and his field notes in another, instead of the pot and ladle filled with food in popular religious iconography.

That both the Goddess of nourishment and Swaminathan, the scientific guarantor of food security, are now relegated in public consciousness is a measure of India’s progress and the liberty we now have to take access to food for granted.

The small, dark godown abutting M Dharmambigai’s large home with a larger courtyard in Kottur, a village 15 km to the south of Pollachi town in Tamil Nadu, has never housed stock so precious.

The value of gunny bags of cocoa beans stacked unevenly, without a great deal of care, is currently more than Rs 12 lakh and almost guaranteed to go up to Rs 15 lakh soon.

The lottery of climate change is such that the misery of farmers in one country is an opportunity to make windfall gains for others in a different continent.

The price of cocoa beans, the primary raw material for chocolate, has more than tripled in the last year. In March 2024 alone, it rose from $7100 a ton to $10455. In fact, chocolate prices now trade higher than industrial metals such as copper.

Can Indian cocoa farmers like her take advantage of rising global cocoa prices?

The following post is contributed by @saiarav from X or Yajnavalkya from Medium

Modi does the unthinkable – goes to polls with a non-populist (revdi-free) budget

At the start of this year, I had written about Modi’s excellent economic stewardship during his second term amidst a period of extreme economic turbulence globally – a once-in-a-century pandemic followed by a major war which roiled energy markets and rapid rate hikes in the West to combat inflation (Modi’s fiscal masterclass). I had noted then that Modi:

“has achieved the near impossible of following a disciplined fiscal policy while not just maintaining his political capital, actually expanding it”

But I had fully expected that he would open up the purse strings during the election year budget this February notwithstanding his public remonstrations against the growing revdi (freebies) culture. And for good reasons. One, Modi had gone in for a ‘revdi’ at the end of his first term in 2019 (the cash transfer scheme for 120 million farmers). And the economic scenario in 2024 was decidedly more mixed compared to 2019 with greater level of economic distress among the poor. Two, recent state elections had seen parties winning based on extremely aggressive freebie promises. For example, Congress won handsomely in Karnataka last year with promises of a slew of freebies (or welfare programs if you like) amounting to more than 2% of the state’s GDP. So I must not have been the only person who was stunned to see that Modi had decided that the normal rules of politics does not apply to him. And as of today, his judgment appears to be spot-on because the only debate about the 2024 elections appears to be what his margin of victory will be. The reasons for this – the so-called “akshat-wave” after the Ram mandir inauguration, the opposition being in absolute shambles, the ever-increasing political stature of Modi – calls for a separate discussion. In this post, I peer into the future and see what Modi’s fiscal statesmanship could potentially mean for the country.

A 10-year long fiscal tapasya….

For reasons that are not entirely clear, fiscal conservatism has been an article of faith for Modi throughout his career as an administrator. He has held on to it steadfastly during his entire 10 years as the the Prime Minister. For anyone familiar with Indian politics, it is easy to appreciate how challenging it can be to stick to fiscal discipline even during times of buoyant revenues. This makes his unrelenting fiscal focus all the more remarkable considering that for most of his tenure, he has been hemmed in by weak tax revenues. Therefore, to call Modi’s 10 year long commitment to financial discipline as a tapasya (penance) would not be out of place.

…might finally yield a Rs.20T (~$50bn) -sized fruit during Modi-3

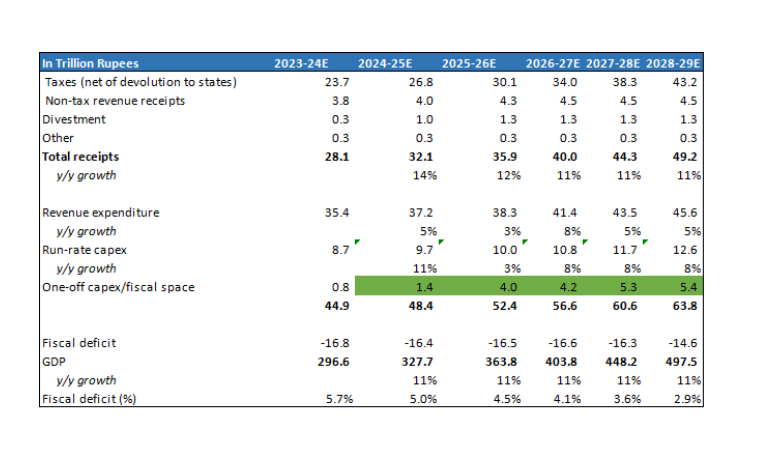

And Modi is on the cusp of reaping the fruits of that tapasya in his third term. Barring unexpected shocks – electoral and economic – he could be presiding over a period where the economy has sizeable fiscal resources to pursue its socio-economic goals; a rare event in independent India’s economic history. Underpinned by a solid cyclical recovery in the economy and strong buoyancy in tax collections (direct taxes likely grew at 20% in 2023-24, twice the pace of nominal GDP growth), Modi-3 is not only placed very comfortably to meets its 2025-26 fiscal deficit target of 4.5% (vs. 5.8% in 2023-24), it will also have its disposal, up to Rs.4 trillion of fiscal space during 2025-26 for spending on new programs or projects (or >1% of GDP) after meeting its regular revenue and capital expenditure obligations. That is the base case which assumes direct taxes grow at 15% annually. In a bull case of direct taxes continuing to grow at 20%, the above figure could be as high as Rs. 5.5 trillion. Further, this figure will continue to swell with each succeeding year as the economy expands and revenue growth outpaces the growth in base expenditure. During Modi’s third term, I estimate that the central government will have up to Rs.20 trillion of aggregate fiscal space for new programs/projects. Also, note that many of the programs of the central government include contribution from the states, which means the total fiscal resources available could be well higher than Rs. 20 trillion.

(For those interested in the math behind the above numbers, I discuss the same at the end of the post) .

Potentially transformative, but availability of funds is not enough

What can one do with an annual budget of Rs.4 trillion? Well, for perspective, the Jal Jeevan Mission which was initiated in Modi’s second term with an annual budget outlay of Rs.0.7T (Rs.3.5T over 5 years, 60% funded by centre) will have provided tap water connections to 160 million households by end of 2024 (110 million connections provided as of April 2024). No commentary required on how transformative this project has been for the 100s of millions of beneficiaries.

In the first two terms, Modi’s focus was primarily on building physical infrastcucture – road building under Gadkari has been an unqualified success while in case of Railways, huge investments have been made, it is still a work-in-progress with mixed results so far. Even welfare schemes had a physical asset bias – from toilets to piped water to housing. While the government deserves a lot of credit for strong execution, it has to be underlined that these are relatively low-hanging fruits from a governance perspective. As the priority areas inevitably shift from road and railways to more complex ones, quality of policymaking, human capital and management will be the key drivers of outcomes, and not just availability of funds. To wit, it is way more difficult to develop 20 high quality IITs or a few hundred Kendriya Vidyalayas compared to building 100K kms of roads. Or just throwing around money into PLIs will not deliver a successful industrial policy.

An opportunity for Modi to cement his legacy – a wide range of focus areas to choose from

What areas Modi will prioritize with the Rs.4 trillion per year (~$50bn) of additional resources is anyone’s guess because this is one government which revels in keeping its plans a total secret. One can only say two things with certainty -one, Modi will be extremely keen to cement his legacy with a couple of flagship projects/programs which has a transformational impact on society. Two, the consummate politician that he is, he will have his eyes firmly on what programs will drive the optimal political benefit for the 2029 elections (and all the state elections over the next few years).

The list of potential programs is endless. Below, I discuss briefly a few ones which I see as critical ones. I classify them into 3 categories: A) long term strategic B) medium term economic growth and C) quality of life. Obviously, most of these programs will tick all three boxes, the classification is based on how a politician like Modi would want to see it. Admittedly, some of the resources might also simply get used up in standard fiscal management as well – ie Modi might simply want to reduce fiscal deficit at a faster pace, or execute the long pending reduction on tax surcharges on the rich or fill up the job vacancies in the government.

Long-term strategic

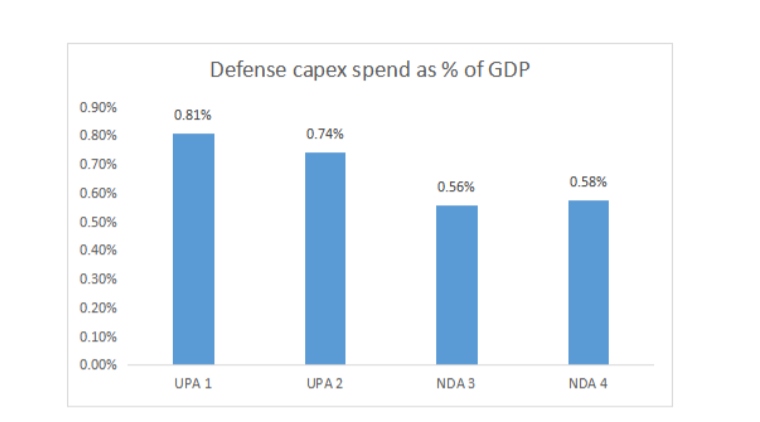

Increase defense capex spend – In contrast to his public image as a hawk on national security, the the spend on defense capex has been rather modest. In fact, as a % of GDP, it has dropped from the levels seen during UPA. With the China threat escalating in recent years, Modi would want to increase defense capex by at least 10 bps (100 bps = 1%), if not 20 bps and get back to UPA levels. That would be 0.35-0.70 trillion increase in annual outlay.

Increased R&D spend – India’s R&D spend is abysmally low at around 0.6% of GDP compared to 2.4% for China. The spend has seen a steady decline from the 2008 peak of 0.9% and private sector has shown very little inclination to spend on R&D with their contribution being only around one-third of the total spend whereas in countries like China and Korea, the figure is more than two-thirds. A key policy objective for the government, apart from increasing its own direct spend, should therefore be to bring in major policy incentives to crowd-in private investments in this area. As it happens, the government has already signaled that this will be a priority area in the third term, announcing a Rs.1 trillion fund to provide long-term interest free loans for R&D work. But much more needs to be done.

Energy security – There are two parts to this. One, as a major importer of oil & gas with demand continuing to grow for the forseeable future, the country needs to own equity in oilfields and LNG plants abroad to enhance its energy security. For example, if India wants to secure say ~20% of the nearly 5 million barrels/d of crude it will import this year, that will mean an investment of $40 billion. Of course, the investment will be done via the government owned oil companies and it will be partly funded via debt. But it might still entail the government infusing a $5-$10 billion of equity.

The second part is investment in energy transition. So far, the Modi government has bet big on solar but now it has also stated its intention of expanding its nuclear fleet (add 15 GW by 2030). While investments in solar power has been largely driven by private players, the government will need to play a big role in setting up nuclear plants. A back-of-envelope estimate for the cost of the plants would be $50 billion and it would be reasonable to assume that the government will have to invest close to half of that amount.

Medium-term economic growth

A PLI-powered industrial policy – An easy prediction to make is that a turbo-charged PLI program will be the topmost priority for Modi-3. After all, the biggest failure of Modi- 1& 2 has been the inability to kickstart growth of the industrial sector and deliver well-paying manufacturing jobs to to a burgeoning labor force. Success or failure to deliver on this during the third term will likely be the most consequential factor in 2029. With the success of the modest sized PLI programs so far, Modi will look to bet much bigger sums on the program. But, at the risk of repetition, PLI itself will not be sufficient. A lot more work needs to be done in terms of improving ease of Doing Business, bringing down land costs, labor laws, building a skilled workforce and so on. One specific area where I really hope Modi-3 focusses on is building a vibrant EV industry (nah, not the two-wheelers, cars are the real deal). We are already a few years behind almost every major auto market globally on EVs. If China is the undisputed leader in EVs today, it is because the government has pumped in nearly $200bn into the industry via subsidies, grants and incentives over the last two decades.

Agriculture – The government would be keen on doing something transformative in this sector, not least because it is still the largest vote bank, but I am not sure ploughing in large sums of money will solve the structural issues bedeviling the sector. Having got their fingers burnt during the second term with the farm laws, it is unclear to me what major policy action they could take up for this sector.

Quality of life

Urban housing and infrastructure – Another easy prediction to make is this (especially urban housing) will be one of the biggest focus areas in the third term given Modi’s penchant for physical infratsrructure. The political dividends will be way higher than what he has received for roads since the change will not just be very visible to the average voter, it will also have deeply positive impact on his day-to-day life. Modi has already delivered well on rural housing but urban housing will be way more challenging, not least due to scarcity of land and a large, ever-increasing migrant population. It will require well-thought out policies and mich greater co-ordiation with the state and local governments

Health and education – The public investment in health and education has been woefully short forever and that trend has continued thru the Modi years. Between the two, I think Modi will focus on health because the political benefits accrue faster and it is also relatively less difficult to execute compared to education. On paper, both these sectors can easily absorb, individually, an additional 0.5% of GDP (I.e. almost the entire Rs.4 trillion fiscal space) given the historical underspend in the sectors. But, more than any other programs, funding is a much lesser factor compared to the ability to build quality organisations which can deliver.

The fiscal math

Assumptions

Nominal GDP grows at 11% (6.5% real and 4.5% inflation)

Direct taxes grow at 15% annually while GST grows at 13%

Divestment (both PSU equity and physical assets) per year of Rs1.25 trillion

Fiscal deficit falls to 4.5% by 2025-26 and below 3% by 2028-29.

A few points:

2024-25E total capex was Rs. 11.1T but this included equity infusions to BSNL and funds for the Science Fund which will not be repeated.

The Jal Jeevan Mission wich has an outlay of Rs 0.7T in 2024-25 comes to and end during the fiscal year, hence lower growth in revenue expenditure in the next year. That, in turn, adds to the fiscal space.

Run-rate capex is for ongoing projects across various sectors – more than half of it is for Roads and Railways. The assumption is that the allocation to the two sectors have peaked and will see more a modest 8% growth growth forward.

Higher growth baked into 2026-27 revenue expenditure to factor in 8th Pay Commission.

The following post is contributed by @saiarav from X or Yajnavalkya from Medium

I flooded the TL with tweets on the budget today. Putting it all together in one place for future reference.

1) The big takeaway — a stunningly non-populist budget in an election year

Unlike in 2019, when the government deliberately advanced the budget date by a month so they could announce a major welfare program (Kisan DBT) and tax cuts for middle class, which added up close to Rs.1 trillion of giveaways or roughly 0.5% of GDP, this budget had almost nothing at all for any section of the voters. This is even more remarkable because A) in the last few years, state elections have seen a strong trend of rampant freebie promises and B) the economic scenario is decidedly more mixed compared to 2019 with clear signs of K-shaped recovery and economic stress in the bottom half of the population. I would have thought Modi would go in for freebies at least comparable to 2019 (0.5% of GDP would be Rs.1.7 trillion), him choosing not to do so is a measure of the supreme confidence he has regarding 2024 elections.

Of course, Modi can still surprise all of us with an unexpected 8 PM announcement with a slew of welfare measures, in which case it will very likely include a large fuel price cut.

2) The fiscal glide path looks very promising; immense possibilities

The budget estimates for 2024–25 are extremely conservative, with some of it to the point of being ridiculous. Take the 2023–24 RE for corporate taxes for example — the underestimate of growth is silly, with just two months left for year-end, it kinda makes the budgeting exercise meaningless.

Overall, I see higher direct tax collections and divestments resulting in at least a 20–30 bps beat over the 5.1% fiscal deficit target for 2024–25. And then we get to 4.0% by 2025–26. This is all very important for the economy — a potential upgrade in our sovereign credit ratings amidst expectation of greater FII investments in the domestic bond market, in turn leading lower interest rates.

The fact that we appeared to have dodged a new freebie program which will be a permanent burden on the resources drives immense possibilities. As the fiscal deficit comes under control, the government will have much greater resources to fund new priorities, beyond road and rail.

The 2023–24 RE for capex spend came in lighter than BE but this is, in large part, because the government shelved the plan for equity infusion into oil OMCs.

The IEBR RE figures were sharply below estimates but this is due to FCI borrowing less funds for its operations (which is a good thing).

One sizeable miss was lower railway IEBR capex — much lower spend on the DFC…apparently because part of the project got shelved.

Meanwhile, Gadkari seems to have no problem handling any amount of capex thrown at his department, solid execution.

For 2024–25, the capex budget is a 10% increase which is pretty good considering its coming off a very strong capex allocation in 2023–24.

4) Huge capital infusion into BSNL — strategic or a waste of taxpayer’s money?

Close to Rs.2 trillion will be infused into BSNL between 2022–23 and 2024–25. This is on top the spectrum it will get for free which as an opportunity cost, if my understanding is right. My initial take was that this was a waste of money into a loss-making, inefficient PSU but then I was told …

…that the capital infusion had a major strategic objective.

5) Defense capex continues to be weak

6) Postal department — yet another case of a broken public sector biz

7) Railway finances continues to be in shambles

I wrote, perhaps two dozen tweets on railways, so I will put that up as a separate blogpost…but the key takeaway, railway finances continue to be in shambles.

8) The difficult job of fiscal management — limited spending discretion

Most of the spend is just completely non-discretionary, minimal ability to cut cost, either for political or administrative reasons.

9) Energy sector capex — disappointing

The IEBR spend by Oil PSUs or capex for atomic energy is modest — remember there was a recent announcement of significant expansion plans in nuclear capacity thru 2030. Well, the money is not forthcoming.

10) What is going on with defense pensions?!? — very low allocation

11) Hits and misses on government spending estimates for 2023–24

The God lording over the oil market has almost always turned a benign eye towards Modi. Oil prices fell by nearly half within a year of him becoming the PM and has stayed moderate for most part of his rule, a big blessing for a a country which depends on imports for more than four-fifth of its consumption. And Modi has used this divine largesse really well, taxing it heavily and testing the limits of his political capital and used these revenues to fund his ambitious capex program amidst anemic overall tax collections. How the timing of oil price movements has been near perfect politically for him can be a separate post in itself; but I will just note that if you had asked an oil analyst in March 2022 where oil prices would be at the start of 2024 if A) the Russia-Ukraine war continued to drag on and B) the developed world saw a period of double digit inflation — his/her answer would likely have been a triple digit figure. But yet here we are, at the start of 2024, with Brent trading under $80.

Petrol and diesel prices stay high despite lower oil prices

So here we are, with oil under $80 and yet the Modi sarkar has not deemed it fit pass on the munificence to the hapless consumers who still have to cough up nearly Rs.100/litre for petrol and diesel, the same level it was in early 2022 when oil had crossed $100/bbl. You might be wondering why I have started with a rambling introduction to get to this point — and I have no reason to offer, except perhaps that I am abusing the munificence offered by Medium, liberated from the character limit from my standard social media app. Thanks for indulging me, dear reader, now I will get down to business, I promise. (Not a good thing to abuse munificence of any kind, which is kinda the point of this post).

A lot of noise, too little light in the debate on fuel pricing

While this issue periodically generates heated debates on X, for the most part, it has been largely ignorant chatter and largely driven by one’s political leanings. And I have not come across any piece in mainstream media which has attempted to shed light on this issue. And that is both astonishing and extremely sad — here is the question regarding pricing of the most important commodity for any economy, and people do not know how it is priced? And we are talking of third largest oil consuming economy in the world here. It is astonishing because oil and its products constitute one of the most transparent, liquid and well understood markets amongst all commodity markets.

So here is my modest attempt to shed a tiny bit of light.

In India, the oil marketing business is largely dominated by oil PSUs who also have a refining business. The business model for oil refining and marketing is pretty straightforward:

A) OMC purchases oil, most of it is imported. The price of oil is linked to Brent, the global oil benchmark. So the refiner pays Brent oil price + ocean freight + insurance. (I am keeping it simple here — the actual price can be a bit higher or lower than Brent)

B) The OMC refines the crude oil in its refineries resulting in various petroleum products — primarily three high value products diesel, petrol and ATF but also propane, naptha etc. The chart below shows the yield of BPCL refineries in 2022–23 — the three high value products account fot nearly 80% of the total output.

C) The products are sold to end customers. For petrol and diesel, which is what this discussion is about, this would mean transporting the products to petrol pumps. Further, the marketed volumes for an OMC could be higher than its refining capacity, which means it will have to buy some part of its products from private refiners (Reliance and Nayara).

The OMCs provide value-add at two stages — refining the oil and marketing the oil and expect to be rewarded for the same. Let us take an example of how that works. First, at the refining stage, the company makes a margin which is the difference between weighted average selling price of all the refined products less the crude landed cost — this is called Gross Refining Margin or GRM. High value products (petrol, diesel and ATF) sell at a price well above the crude oil price while a product like Naphtha sells for less than the crude price. But keep in mind, the high value products account for 80% of volume and hence driven the GRM. As the term implies, this is just the ‘gross’ margin and the company obviously has operational expenses during the refining process.

At the marketing stage, the company would expect a margin for maintaining a retail network and transporting the products to the dealers. And of course, there are costs of marketing the products as well. As of 2019, the per litre marketing cost + margin was Rs. 2.0–2.5 per litre (source: page 60 of this Petroleum ministry report). So let us say, its Rs. 2.7 currently accounting for inflation. The unit of measurement will keep shifting from barrels to litres, so you might want to keep in mind that 1 barrel = 159 litres.

Continuing from the above table, let us say, the OMC sells petrol at the refinery gate at a price of $92 (which would be refining margin of $9/bbl). Adding in a marketing cost of $5, the price to the dealer would ultimately come to Rs. 50.9/litre.

Adding to the price paid by the dealer, we then have the central and state government taxes and the dealer margin. Currently the price build-up for petrol and diesel (for Delhi) stands as follows:

Note that the price at which it is sold to the dealer is Rs.57–58 which implies a per barrel price of $109–110 while Brent currently trades at <$80. Since the marketing cost & margin is fixed, that means, the OMCs are getting a refining margin of $20+/bbl on both petrol and diesel.

Is $20 high, or is it low, or is it normal? Below is the chart of BCPL’s GRM for the last 8 years. Note that this is the GRM for its entire set of product and petrol and diesel margins will be a couple of $ higher.

Typically, OMC GRMs have averaged mid single digits and the last two years, and especially FY 22–23 were outliers.

But what is the official pricing policy?

In theory, petrol and diesel prices are deregulated which means prices track the global prices for the two products (which is simply Brent price + regional refining margins). But it does not take an oil market expert to figure out that the policy has been quietly buried since early 2022.

The pricing is arrived at by what is called the Trade Parity Price (TPP) which is the weighted average of Import Parity Price (IPP) and Export parity Price (EPP) weighted in the 80:20 ratio. IPP simply means what is the theoretical price at which petrol or diesel can be imported to India ( we do not need to import since we have surplus refining capacity) — that price is basically the one at which refiners in our region will find it attractive to export to us. In other words, IPP for petrol and diesel is based on the refining margin of the two products in our region. The same concept applies for EPP — it is the price at which one can export which is linked to refining margins in the key export markets. Typically, the margins in Singapore market is used as the benchmark. And that explains why refining margins shot up in the last couple of years.

Underrecovery ….or how OMCs made bountiful GRMs but little money in FY 22–23

A $20/bbl GRM in FY 22–23 should have been a major cause of celebration for OMCs but it was not for the simple reason that the GRM was a notional number. For all of FY 22–23, the OMCs were selling petrol and diesel at Rs.57–58/litre to the dealers which is roughly around $110/bbl. Now considering Brent averaged $95 during the year and shipping costs had shot up during the year, this is how BPCL’s overall margins would have looked for petrol assuming a $22/bbl margin. Remember that the company is supposed to make $5.15/bbl towards marketing margin and costs. Instead, they incurred a loss of $11/bbl. And that is what OMCs, quite morosely, term as underrecovery. In reality though, the company did make a combined refining & marketing margin of $11/bbl but if one assumes refining and marketing costs of, say $8–9/bbl, they made very little in terms of cash profits from sale of petrol. There is also the further angle that they would have had to purchase some portion of petrol and diesel from Reliance and Nayara at global prices (ie $95+$4+$22 = $122) and sell that for $110. And on top of that, they had to incur huge losses on LPG cylinder sales, so yea overall a tough year, but I digress. The case that BPCL will be putting forth to the government is that they made $16/bbl underrecovery on petrol and diesel in FY 22–23 and they should be allowed to recoup those “losses” — my rough estimate is that that amounts to Rs.25,000 crores to be recouped!! To put this number in perspective, BPCL annual profits have averaged 8–12K crores in the past and the company is asking that they be allowed to make 25–30K crores for FY 22–23 because, hey, GRMs were so high.

So what is a reasonable GRM for OMCs?

Singapore refining margins for petrol and diesel are currently around $10 and $20 respectively. So if one goes by that figure, diesel should be around Rs.55 to the dealer might well be justified while petrol price should be around Rs.51. As a reminder, the current price to the dealer is Rs.57–58.

So even based on market pricing, there would be a case for cutting the petrol price. Of course, the question that arises is what about the losses incurred in FY 22–23, which I will come to later. But I would argue that the government has anyway jettisoned their pricing policy and should therefore stick to that changed stance and just view it as what is a reasonable GRM that the OMCs should be getting. I would say, $6.5/bbl is a pretty healthy margin. Or stick to the current pricing policy and slap a windfall tax (just like they do on exports of refined products).

One counterargument to this is that OMCs have ambitious growth plans and these high GRMs will be really helpful. In my view, they should just be asked to borrow money.

In the next section, I discuss what the potential for cutting prices is.

If we go strictly by the official fuel pricing policy, then BPCL needs to be allowed to recoup its underrecoveries of Rs.25K crores, so any cut is out of question, for this year, or the next, or maybe even the one that follows — and that is asuming oil does stay at $80. Or Modi could request BPCL to be let bygones be bygones — and I am sure the BPCL CEO, as a good corporate citizen, will give it a sympathetic hearing — and ask them to adjust the price down to current TPP levels, in which case, as I have pointed out earlier, there is scope to cut petrol prices by >Rs.5/l and diesel by a couple of Rupees. Votaries of free market can stop reading at this point because as I had suggested in the previous part, the government should just tell the OMCs that they stay happy with a GRM of $6.5/bbl. That would be $8.5/bbl refining margin for both petrol and diesel.

If we go with $8.5/bbl, then what would be the price to the dealer? I am assuming Brent price of $80/bbl though prices have generally remained a few dollars below that level over the last few weeks. Also note that since a large component of our imports are now discounted Russian crude, the average import price should be below Brent ( we also buy cheaper quality, lower price crude vs Brent generally, but not getting into further details). At $80/bbl and $8.50/bbl of refining margin, we can potentially reduce prices by Rs.6–7/litre. But there are two factors which need to be considered as well, one positive and one negative — the OMCs are sitting on huge surplus profits built up over the first nine months of FY 23–24. On the other hand, the OMCs are currently selling LPG cylinders at a loss.

How much surplus profits have OMCs build up?

Let us look at BPCL’s financial performance since the start of FY 22–23. Excluding exceptional items, the company’s profits during FY 22–23 would be around Rs. 5–6K crores. This compares to historical annual profits of Rs.10–12K crores. So that would mean a loss vs historical average to be recouped of, say Rs. 5K crores (not the insane underrecovery figure of Rs.25K crores or ~Rs.20K crores post taxes). How much after-tax profit did BPCL make in 1H 23–24? Rs.19K crores!! Yes, you read that right — they made 1.5x in 6 months vs their peak annual profit historically. If we consider Rs. 13K crores as reasonable profits for FY 23–24, they have already achieved it *AFTER* recouping their losses for FY 22–23. In other words, even if they do not make another Rupee for the rest of the year, they would be fine. But given benign oil prices in Q3 , they should be making outsized profits in Q3 as well. Short point: the company is sitting pretty as far as profits go.

While I have not analyzed the other two OMCs in similar detail, the profit performance broadly follows the same trend as BPCL, as is to be expected.

Losses on LPG sales, possible combinations for price cuts

At current global LPG prices, OMCs are making a loss of between Rs.150–175 per cylinder sold. The OMCs have made humongous surplus profits from LPG sales in 1H 2023–24 — as per this article by Devangshu Dutta, those profits are not recorded in the books, the surplus profits are instead placed in an adjustment account to offset future losses. Mr. Dutta estimates the fund has accumulated Rs.12K crores by end-September. I will leave out this part in my analysis since there is no disclosure by OMCs in this regard but if true, it provides further upside to potential price cuts.

At $80 oil price, this is how I see surplus daily profits earned by the OMCs in aggregate. They collectively make Rs. 1.89 billion of surplus profits every day.

So a price cut can follow any of the following combinations. Politically, a sharper cut in petrol and LPG prices is more preferable ahead of the elections (scenario 2 and 3) while a cut in diesel prices would be better for battling inflationary pressures. And there is upside to these price cuts if one considers that the OMCs are sitting on large surplus profits this year so far. My own preference would be somewhere between scenario 1 & 2 but I would definitely not grudge Modi dipping into the OMC’s surplus proifts and going for a bigger cut. Of course the risk in that case is he will need to revert to more normalised prices by the end of this year. Or horror of horrors, bring down the fuel taxes.

I would like to highlight that I consider these cuts as the floor estimates considering assumptions for the price build-up are quite conservative, whether it be on crude oil landed cost or marketing costs and margins. Apart from the fact that OMCs are already sitting on huge surplus profits.

Postscript: I have grown tired of explaining why these price cuts have no impact on the fisc. As you can see from the analysis above, price cuts do not require even a single Rupee of tax cuts by the centre. Currently, all the surplus profits are just flowing into OMC’s Profit & Loss account.

Appendix — LPG cylinder price math

Source: based on this 2017 PPAC report — domestic costs in 2017 was Rs.120. Should possibly be currently in the range of Rs.150–175 after accounting for inflation

In the run up to Indian parliamentary elections in 2024, there is excitement in some sections of social media about “freemarket” ideas espoused by C Rajagopalachari (Rajaji) and the Swantantra Party he helped found in 1959.